Paintings, precious stones, watches and jewellery, wine, leather goods, collector’s vehicles, various art collections… each of these special items comes under the heading of Fine Art & Collectibles. This is an area that normally requires several experts to be brought together to appraise the goods and determine their value. At PSPI, we take care of everything thanks to our Fine Art & Collectible department, headed by a specialist in insurance law and an art object expert.

We manage the precious assets entrusted to us on a global basis, from the inventory, to determining their value in real time, to their insurance cover.

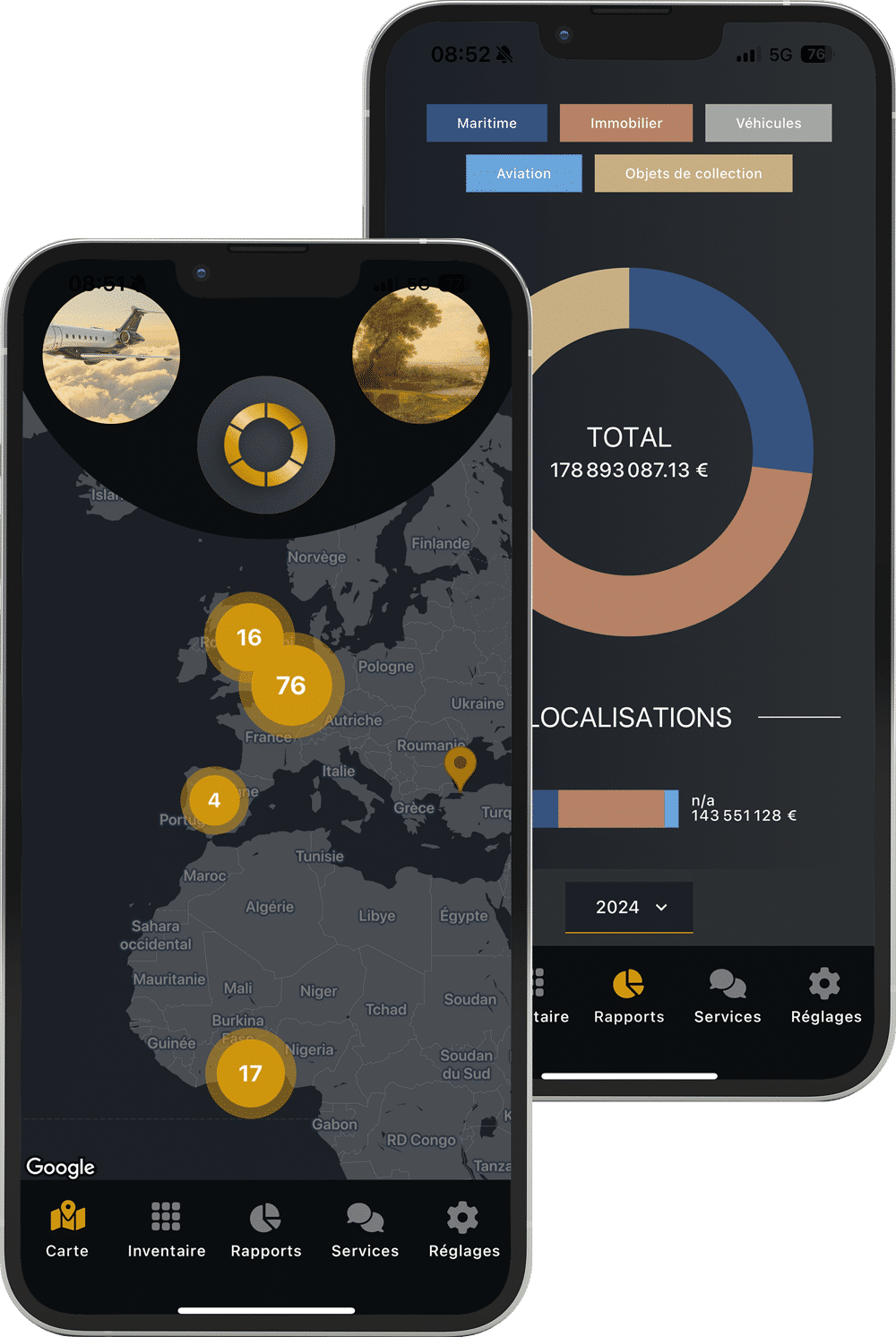

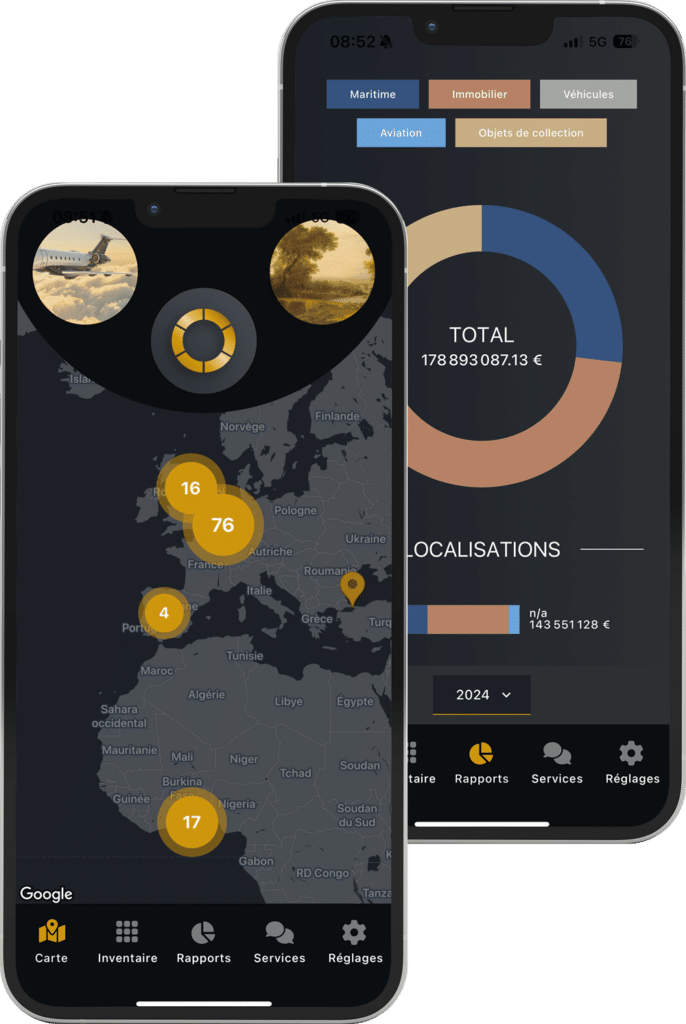

On the customer’s side, all their physical assets are visible at a glance – the value of the assets individually and cumulatively, their location, etc. – via the PSPI Application.

If mobility is everyone’s concern, having the guarantee of health insurance that goes beyond border considerations is a real challenge. That’s why we decided to create a unique, comprehensive and simple product: international health cover valid anywhere in the world. Treatment can be received in any country, with full access to world-renowned hospitals, clinics, doctors and specialists.

The range can be customised for each individual, family or international group, and is valid for all profiles regardless of nationality or country of residence.

We offer you a unique service, with global management of all your property, regardless of the country in which it is located. In short: a single insurance contract for all your property, for greater convenience, lower costs and monitoring at all times.

Fully customisable, the insurance contract is designed to protect all your property, valuables and collections. We guarantee protection for all the contents of your home against the risks of fire, burglary, water damage, glass breakage or natural disasters.

And thanks to our Application, you can see at any time the rental and/or purchase value of your possessions, their location, and their weight in the total value of your assets.

For owners of yachts and/or aircraft, we have created a comprehensive insurance programme and a tailor-made approach that meets all the needs of owners of these luxurious assets and covers all the potential risks involved.

We have teamed up with an international team of marine and aviation specialists, selected for their proven track record. As a result, we are able to insure everything on these properties, from equipment, on-board assets and passengers/crew, to the management of all potential risks.

Via the PSPI Application, you can find out at any time where your yachts and/or aircraft are located, and what their individual value is, as well as their value in your estate as a whole.

The protection also extends to individuals, in their daily lives, when travelling, and even in the event of unforeseen events. Protection that extends internationally, wherever you are, and is valid for all members of your household.

Life insurance, travel insurance, legal protection, kidnap and ransom, third-party liability (TPL) – we take care of all the insurance that private individuals need.

We have the privilege of offering a complete range of tailor-made products to meet all your insurance needs, in Switzerland, Europe and throughout the world.

Professional insurance solutions for the Financial Line, Real Estate and Corporate sectors.

Over the last few years, I’ve seen the behaviour of some of our customers change and evolve. Rather than remain anchored in the model we used 15 years ago, we have decided to follow them. And so we embarked on our “insurance springtime”.

Today, our customers don’t just want advice, they also want to be involved in managing their assets and their portfolios. They want to understand and closely monitor their assets, and to have a genuine, transparent dialogue with the experts that we are.

To achieve this, an innovative vision is not enough. We need to be able to change the way we operate, the way our services and expertise are presented.

This is where our PSPI application comes in. Customers now have access to a complete map of their assets, in real time, with a constant update of all their assets and their insurance management carried out by our experts.

This Applicationopens a new chapter for PSPI. A chapter that will challenge our sector even more, much to my delight.